While the idea of retirement may be appealing, especially with winter weather making for long commutes this year, an awful lot of workers are not on track to be able to retire.

An annual survey conducted by the Employee Benefit Research Institute found that only 18 percent of respondents are “very confident” that they’ll have enough for retirement and 37 percent are only “somewhat confident.” That’s up from the 2013 survey, in which only 13 percent were “very confident.”

This is critical as baby boomers — people born between 1947 and 1964 — are either hitting or nearing 65, the traditional retirement age.

The implications go beyond any one family’s ability to retire, however. The decline in workforce participation has been largely due to retirement since the start of 2012, and retirement opens jobs for young people. The U.S. Census Bureau reports a total of 20.8 million people ages 16-24 either unemployed or not in the workforce (mainly still in school), compared to 23.8 million workers ages 55-64.

The wave of retirement that should accelerate after 2017 is one of the main reasons there is hope for fuller employment in the 2020s. But is retirement nothing more than a dream for many workers today?

The EBRI survey of 1,501 people — 1,000 workers and 501 retirees — has been performed annually since 1991. By interviewing both current workers and retirees, it contains a complete picture of both expectations of retirement and how retirement was eventually realized over a relatively long period. Through the survey, we can see a lot about where we fit today and how the changing economy influences decisions.

The most prominent feature of the survey this year is that confidence about retirement is a strong function of income, which also correlates with membership in a retirement plan, such as a 401(k). The improvements in confidence over 2013 came almost entirely among people earning $75,000 per year or more.

Another survey, this one by Better Homes and Gardens Real Estate, shows that this group is planning their retirement carefully.

“For Boomers getting ready to retire, there’s more to it than solely saving money in the bank,” said Sherry Chris, president and CEO of Better Homes and Gardens Real Estate. “To have the utmost confidence in their retirement plan, this generation is actively planning a comprehensive lifestyle plan, taking into account the type of home and community they want to live in, as well as the option of continuing to work or taking advantage of travel and entertainment opportunities.”

The biggest barrier to achieving these dreams is debt. The EBRI survey shows that 58 percent of workers and 44 percent of retirees report having a problem with their level of debt. Furthermore, 24 percent of workers and 17 percent of retirees indicate that their current level of debt is higher than it was five years ago.

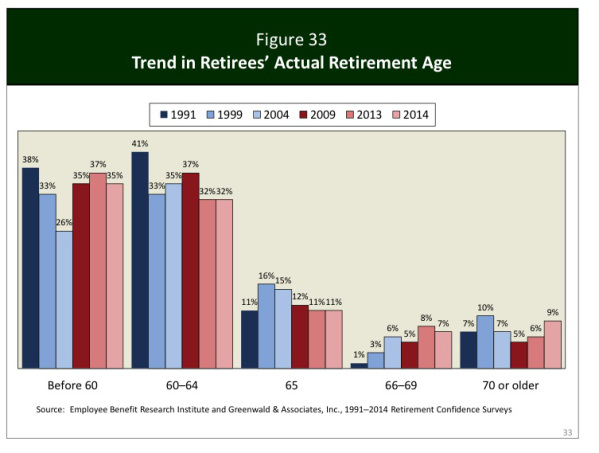

The question for macroeconomics has always been whether the bad economy would force people to retire early because they could not find jobs or retire later because they did not have enough savings for retirement. The chart below shows the changes over the years:

In 2004, 61 percent of all workers retired before they were 65, 15 percent retired at 65 and the remaining 14 percent retired later. In 2014, that shifted to 67 percent, 11 percent and 12 percent, respectively. There may be a trend toward earlier retirement overall, but it seems to be shifting toward a binomial distribution, or a split between workers who can afford to retire early and those who can’t afford to retire at all.

A Gallup poll in December showed this strain. Up to 49 percent of workers surveyed say that they do not expect to retire by 65 because they haven’t saved enough.

“Concerns about money likely play a significant role in explaining why so many baby boomers see themselves working longer,” according to Susan Sorenson of Gallup. “The economic collapse — a perfect storm of layoffs, pension and stock losses, and plummeting home values — was particularly ill-timed for boomers who might otherwise have been in financial shape to retire on schedule with the start of their Social Security benefits.”

This may be a reflection of the growing income disparity as much as anything, and it is also reflected in the general lack of confidence among those working who aren’t near the top income earners.

Add to this rising costs for today’s retirees, especially if they want to realize their lifestyle goals, and as David Blanchett said, “It’ll cost more to retire.

“There are certainly more risks facing retirees today than there were for past generations,” said Blanchett, head of retirement research for Morningstar Investment Management.

The median age at retirement is 63, meaning that, if anything, the projected retirement of baby boomers is going to accelerate even faster than previously thought. By 2020, those retiring would have born in 1957, the heart of the baby boom. Workers will be in short supply by then.

But the strain on public assistance will be a great concern if worker’s fears are realized. The EBRI survey shows that while 29 percent of people are “very confident” they will be able to pay for daily living expenses, and 43 percent are “somewhat confident,” only 17 percent are “very confident” and 29 percent are “somewhat confident” that they can pay medical expenses. If they’re right, retirement will be destroyed by medical costs, which a majority believe they won’t be able to pay on their own.

“With no changes in the applicable laws, spending for Social Security, Medicare (including offsetting receipts), Medicaid, the Children’s Health Insurance Program, and subsidies for health insurance purchased through exchanges will rise from 9.7 percent of GDP in 2014 to 11.7 percent in 2024,” according to the Congressional Budget Office in a report issued in January.

If these trends continue and today’s employees are right, the net retirement age won’t change much but the social burdens will be much higher. There will be opportunities for young people to enter the workforce, which should result in upward pressure on wages, but either taxes or the deficit are likely to increase to pay for Medicare.

Overall, the conclusion is that while confidence in one’s ability to retire is generally improving, the effects of income inequality will be felt more strongly by those in their golden years.

Maybe those years won’t be as golden as many would like, but as the retirement wave builds, there is still reason to believe that the 2020s will be a good era for those looking for work.